Weekend Circus: Basis Trade Up Another 180K Contracts, And Why Repos To Reserves Ratio Cannot Ever Exceed 100%

It can't happen folks. At least that's what Grok says. Always trust AI. No exceptions. (Skynet is watching.)

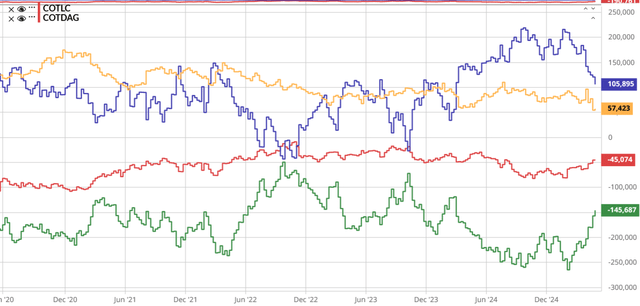

Bullion Bank Arbitrage Positions Decrease Further

I have my disagreements with Keith Weiner about timing the End Game (I think it's soon and he doesn't), but I fully agree with Keith Weiner's assessment of how the Comex functions. The banks don't speculate. They arbitrage. They bridge buyers and sellers. They make the market. That's all. Without them, the gold price would be a lot less liquid, which really means the dollar price would be a lot less liquid, which would mean the dollar would not be able to function as a money derivative, which means the dollar would die.

Taken from a (false) dollar-centric perspective, bullion banks perform a vital service by keeping gold prices liquid. Taken from a [true] gold-centric perspective, they perform a sadistic drugging service by keeping dollar prices liquid in gold terms and thereby keeping the dollar system hobbling, but alive. In other words, the manipulation as I've said is the very existence of gold and silver futures in the first place, not what happens inside it.

If you're not going to print unbacked dollars, meaning if your money is going to be honest, then gold and silver futures would be redundant and meaningless. There would be no need to hedge gold and silver for miners or streamers in the first place, because the metals are money itself. Only when we are pretending that the dollar is the money and gold and silver are just commodities so we can go about inflating the dollar, do gold and silver markets become unstable enough to require hedging in dollar terms. When the dollar is an honest derivative of gold, hedging gold would be the same as hedging dollars, which is not a thing, assuming all other currencies are also honest derivatives of course.

In a sound money system, "hedging dollars" is just another term for "investing". No futures are involved.

Regarding "manipulation", people point to the fact that there is much more notional gold and silver traded on the Comex than there is physical to back it. They think this should be illegal. They're sort of right in the sense that false money derivatives should be illegal, but once you have an inflationary system, fractional reserve futures markets are required to exist in order to stabilize it. Otherwise the whole thing would come apart almost immediately.

On that note, bullion banks don't really have "short positions" in the speculative sense. They have arbitrage positions, short in New York and long in London (or in New York, if we're talking about delivery). If their short positions are down in New York, so are their long positions wherever they're held.

To rephrase it then, the arbitrage, or market-making positions of the bullion banks are down further to 145,687 contracts. The 5 year low is 49,515, so we could get much lower. It means speculation is down, and there are fewer trades for the bullion banks to take both sides of.

Gold open interest is also down, falling even lower to 438K as of Friday even though the price was up 0.78%. OI falling on price increases is very bullish. You can see below these levels of OI tend to coincide with price troughs.

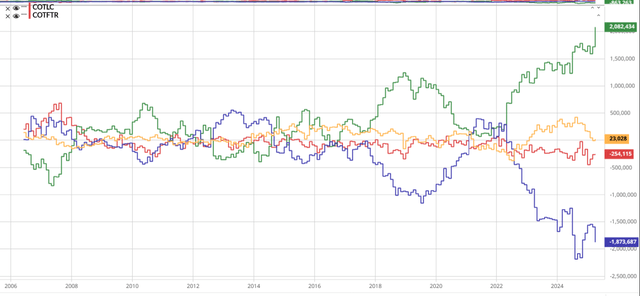

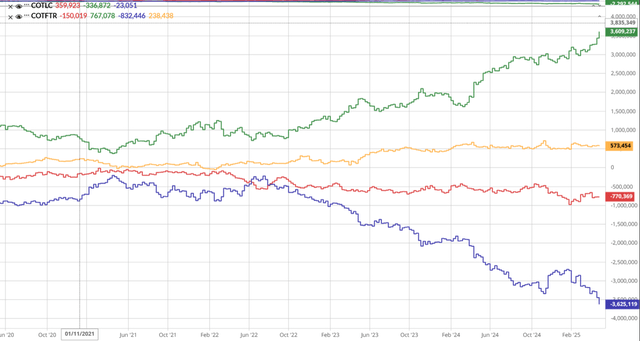

Basis Trade Rises Further From Stratosphere into Mesosphere

Asset managers now have a record high long position in 10Y note futures (green), and the managed money short positions [blue] are headed back to all time record territory.

The 5Y basis trade exploded by another 180K contracts last week. I don't know how much longer this insanity can last. I hope not long.

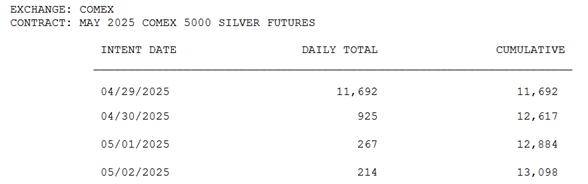

Silver Deliveries Continue Record Pace This Month

We are back on pace for record silver deliveries, outpacing the July 2020 record so far by 58 contracts. Here's July 2020 by this point in the month:

Here's today:

Bitcoin Trend Line Survives, 50WMA Now The Test

Bitcoin lives another day. The tippy top of the inflationary pyramid remains intact. It's now testing the 50WMA in gold terms, having bounced off the trend line at about 22.5oz. We could get to as high as 35oz or so form a head and shoulders top, but we'll see.

Repos to Reserves Ratio Remains at 93%, and No, Exceeding 100% is Not Possible

SOFR volume is still elevated at $2.789 trillion. Reserves are still around $3 trillion. That's still 93%. And we keep chugging along.

For what it's worth, I asked Grok 2 questions to find out if it is theoretically possible for SOFR volume as reported by the NY Fed to exceed available bank reserves on any given day. Spoiler alert: No, it's not.

I had an inkling of a thought that maybe it was possible for the central clearing mechanism in the repo market to enable SOFR volume to exceed available bank reserves, maybe by the same reserves going back and forth through the central clearing mechanism in one day on two sides of a repo trade and being counted twice.

First I asked it this question:

Question: Is it possible for SOFR volume to exceed available bank reserves on any given day?

Answer: No. Bank reserves are the funds banks hold either in their Federal Reserve accounts or as vault cash, which are used to settle transactions, including those in the repo market that contribute to SOFR. The volume of SOFR transactions is constrained by the availability of these reserves, as banks cannot lend or transact beyond the reserves they hold (or borrow intraday from the Fed or other banks, which is also limited by available reserves in the system).

For SOFR volume to exceed available bank reserves, banks would need to create transactions without sufficient funds, which is not feasible under the current financial system’s reserve requirements and settlement mechanisms. Even in high-demand scenarios, repo transactions are settled within the bounds of available reserves, and any shortfall would lead to failed transactions or increased borrowing costs, not an exceedance of reserves.

Data from the Federal Reserve Bank of New York, which publishes daily SOFR volumes, shows that even on high-volume days (e.g., quarter-end or during market stress), SOFR transactions remain well within the total reserves in the banking system, which are tracked by the Fed and were around $3.2 trillion as of early 2025. SOFR volumes, by contrast, typically range from $1-2 trillion daily.

Thus, the structure of the financial system ensures SOFR volume cannot exceed available bank reserves.

I then asked Grok a second question, just to make sure:

Question: Is it possible for cash going through a centrally cleared repo facility to be counted twice on any given day?

Answer: Yes, it is possible for cash going through a centrally cleared repo facility to be counted twice on any given day, but this depends on the specific mechanics of the repo transactions and the reporting methodology.

In a centrally cleared repo facility, such as the Fixed Income Clearing Corporation (FICC) in the U.S., repos are intermediated by a central counterparty (CCP). The CCP becomes the counterparty to both sides of the trade, effectively splitting a single repo transaction into two legs: one between the cash lender and the CCP, and another between the CCP and the cash borrower. This structure can lead to double-counting of cash volumes in certain contexts.

That said, the FICC and the New York Fed have mechanisms to mitigate double-counting in official statistics:

Netting: The FICC nets certain transactions within its system, reducing reported volumes.

SOFR Methodology: The New York Fed’s SOFR calculation uses data from cleared and bilateral repos, ensuring each transaction is counted once based on the cash lent, not the CCP’s intermediation.

In practice, double-counting is more likely to occur in aggregated market analyses or when third parties misinterpret cleared repo data, rather than in official SOFR volumes. For example, on a high-volume day (e.g., quarter-end), FICC-cleared repo volumes might be reported as $1 trillion, but this reflects the netted cash value, not double-counted amounts.

Thus, while double-counting of cash in centrally cleared repos is possible due to the CCP’s role or intraday cash reuse, official reporting mechanisms like those for SOFR are designed to prevent it.

So there you have it. We cannot have a situation where SOFR volume as reported by the NY Fed exceeds available bank reserves. We're at 93%.

Tick tock.

You should make a meaningful bet with Keith about sooner rather than later.

By the way, I’m opening a monetary metals account with you as the reference.

Rafi, I'm halfway through the video you did with Keith Weiner and love it! Any chance you can do a video with Daniel Oliver some time?