Guy In Charge of Fed System Open Market Account says Everything's Awesome While Playing Building Towering Lego Pyramid

And gold open interest likely to take a huge hit towards 400K today as China Trade War Takes a Time Out

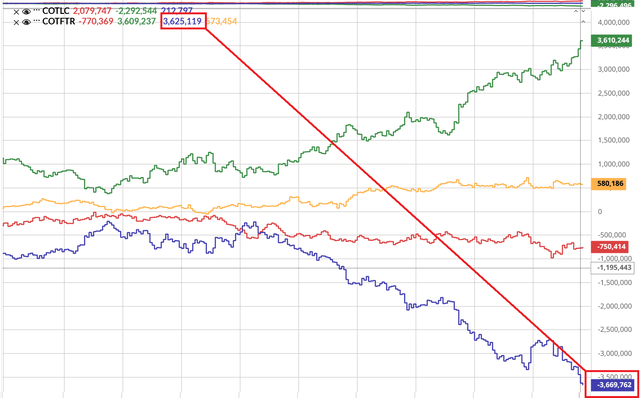

2 Biggest Basis Trades Continue to Grow Fast

It's the 5Y and 10Y basis trades that are piling up week after week. The 10Y basis trade – where hedge funds profit off of a slightly higher futures price for 10Y notes than for the actual paper and multiply by borrowing in the repo market – is up past 2M contracts, or 11% for the week. We are nearly at a record high here. In the graph below I show the current level and last week's connected by the red line.

The 5Y Note basis trade is even more extreme, up to a new record 3.669M contracts, or 1.2% for the week. 5Y Notes have by far the biggest basis trade on them.

On the topic of the basis trade, a subscriber sent me Roberto Perli's speech last week. He's the guy in charge of the SOMA account, the System Open Market Account, which is the mechanism that buys and sells securities for the Fed on the open market. Perli said the following on the basis trade.

The total volume of basis trades is estimated to be large. In March 2025, leveraged funds’ notional value of short Treasury futures positions with maturities up to 10 years—one rough proxy for hedge funds’ basis trading volumes—stood at about $1 trillion, well above levels observed in February 2020. The sudden unwind of those trades could have been an additional and significant source of market instability due to associated selling pressures that could have overwhelmed dealers, whose balance sheet capacity was already limited.

Nothing surprising here. He's just stating the obvious. Then we get to this, and it's a tail wags dog type of logic:

One factor that could lead to a rapid unwind of the basis trade is substantial repo rate volatility or a persistent increase in repo rates, which could in turn increase the cost of financing the position and therefore make it unprofitable. But this by and large did not happen in April since repo rates were fairly stable and dealers remained willing and able to intermediate. As a result, according to Desk staff’s estimates, the basis remained relatively stable. This stands in sharp contrast to March 2020, when the basis jumped by about 100 basis points and the unwinding of basis trades was likely an important contributor to the sharp dislocation in the Treasury market we observed at that time.11,12

In other words, the wet streets cause the rain to fall, the tail wags the dog and so forth.

In reality, higher repo rates do not "cause" the basis trades to unwind. Higher repo rates are a symptom of dollar scarcity in the repo market, which causes basis trades to unwind because there aren't enough dollars to fund them. They are unwound by margin calls which force the firms engaged in the basis trade to sell something usually completely unrelated (say Nvidia stock or whatever) in order to comply the margin call (if they don't, the broker will force sell

Keep reading with a 7-day free trial

Subscribe to The End Game Investor to keep reading this post and get 7 days of free access to the full post archives.