Debt Ceiling Wrench - The Plumbing Picture Just Got A Lot Weirder

And Bitcoin, to my chagrin, makes a new high in gold terms. But can it survive a dollar crunch banking crisis? If it can, I was wrong. But I'm betting it can't.

The debt ceiling will be hit on January 2. That means Treasury will start spending down its checking account, the TGA, which increases bank reserves.

It also means Treasury will cut T-Bill issuance, and some cash from T-Bill redemptions will have to go back into RRP instead, which decreases bank reserves.

The two processes should cancel each other out more or less, and QT will continue to shrink bank reserves on net until a crisis hits.

Bloomberg notes the danger of the bloated basis trade in triggering a chain reaction that nobody knows the effect of.

Bitcoin makes a new high in gold terms. But can it survive a banking crisis? If it can, I was wrong. But I don’t think it can.

I’ll start with Bitcoin. Yes, it made a new high in gold terms, and I was wrong in saying it wouldn’t. Again, I’ll be honest and say I still cannot see how logically it can possibly be money. If there’s no logical foundation, then at some point it’s got to crash in real purchasing power.

If bitcoin survives the next dollar crunch without plummeting wildly in gold terms, then somehow, it must be money, or at least a good money derivative. Many people are thinking the question has already been answered, and bitcoin is here to stay. I say it will be answered during the next dollar squeeze. So here’s the latest on that.

A critical article was just published in Bloomberg that throws a real wrench into the monetary plumbing. It's what you could call a plumbing slingshot incoming. There are many moving parts here and I don’t quite see how they all move together myself, so I'm trying to work it all out as I write this.

Bloomberg notes:

The debt limit will be reinstated on Jan. 2, prompting the Treasury Department to deploy a series of extraordinary measures that include spending down its cash pile and reducing the amount of T-bills it issues to preserve its borrowing capacity.

So on January 2, the "extraordinary measures" begin because of the debt ceiling. That means the Treasury spends down the TGA and shrinks the amount of T-bills offered, in order to keep outstanding debt below the statutory limit. Bloomberg continues:

Because the Treasury’s cash balance, known as the Treasury General Account, or TGA, is one of the major liabilities on the Fed’s balance sheet, such measures will boost mainly bank reserves parked at the central bank and demand for the overnight reverse repurchase agreement facility, or RRP. That means markets will be flush with cash as the Fed continues shrinking its own balance sheet in a process known as quantitative tightening, or QT.

I don't think this is correct. I don’t think bank reserves will be boosted because the spending down of the TGA, which does increase reserves, gets cancelled out by the cutting of the T-Bill supply because the money that would have gone into the TGA when a money market fund buys a T-Bill, instead goes back into the RRP facility. So in other words, see this table from the H41 Fed balance sheet release:

Whenever the "Total factors, other than reserve balances, absorbing reserve funds" goes up, the "Reserve balances with Federal Reserve Banks" goes down, with the difference between them being QT. But since the blue rectangle will go up by the amount that the red rectangle goes down (more or less), total factors remains more or less steady, meaning so do reserve balances.

Thing is, the money that goes back into RRP because of the cutting of the T-Bill supply thanks to the debt ceiling, is pretty much stuck there and can't go anywhere else. So those dollars will be unavailable for anything. They can't help grease the repo markets because, as Bloomberg puts it (my bold),

Given that it’s likely the Treasury will have to reduce its bill issuance until the debt cap is raised or suspended, money-market funds will be motivated to park more cash at the RRP despite higher private repo market rates. There were similar frictions in July when dealer balance-sheet constraints and sponsored repo limitations kept usage of the reverse repo facility sticky.

“Capacity constraints, as well as counterparty risk limits have potential to push money market fund cash into the RRP,” impeding the liquidity redistribution process,” Tobias wrote. “This in effect reduces the supply of repo financing at a time when demand” is continuing to increase.

So we will see RRP increasing again, as cash drains out of the TGA balancing out reserves, but no more money than otherwise will be available for daily repo transactions. I think the chart below can explain visually what I think is going to happen. The red line (TGA balance) will go down, the green line (RRP balance) will go up, and the blue line (reserves) will move by about the difference between the change in the green line and change in the red line.

Then what happens is the debt ceiling gets resolved just as the TGA empties. Most of the G-SIB banks believe that the debt ceiling resolution happens at the end of March, two months into Trump's term. What happens at that point is that RRPs go back down and refill the TGA. Meanwhile, as this zig zag continues, reserves continue to fall due to QT. Here's how Bloomberg puts it, quoting head of interest rate strategy at TD:

“The Fed may be flying blind in monitoring the impact of QT as the debt ceiling starts to pressure TGA balances lower, temporarily increasing reserves in the system,” said Gennadiy Goldberg, head of US interest rate strategy at TD Securities. “This also increases the risk that once the debt ceiling is raised and the TGA sharply increases, reserves are drawn down quickly and lead to outright scarcity.”

…any rebuild of the TGA will result in a drop in bank reserves. Although the account is currently at $3.23 trillion, a level policymakers consider abundant, market observers are closely tracking the level to assess at what point it will become scarce.

Not only that, but Bloomberg even takes note of the exploding basis trade, which is still at astronomically high levels (my bold):

In addition, there’s a greater risk of more volatility because the backdrop of the funding markets is different than last time, according to Morgan Stanley. Since 2023 there’s been a “significant increase” in hedge funds’ long Treasuries positions, with even more collateral sitting outside the Fed and banking system, strategist Martin Tobias wrote in a year-ahead note.

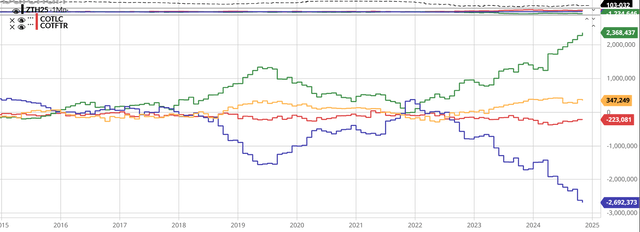

What that's talking about you've seen here many times. It's this chart below of 2Y Treasury futures positioning. The "significant increase" since 2023 is obvious, and it keeps getting worse:

You can tell pretty easily that the funding for these "hedge fund long treasury positions" is coming from repo because the SOFR volume (below) rises at the same time the blue line (above) goes down, starting in 2023:

Exactly how all these crazy factors trip over one another to trigger the final monetary earthquake we do not know. All we know for sure is that it will. And when it does, we will all know it. Then we can all write papers about how it happened and such, assuming we're not all roaming around shooting zombies with shotguns.

As everyone knows, Bitcoin was conceived as a decentralized payment system but has since been rebranded as a store of value. Its price has been propelled higher by demand created by new centralized and financialized derivatives.

The more I think about all of the elisions of truth surrounding Bitcoin the more it seems to me that it cannot be money. Money has to be the most stable and most liquid of commodities. Bitcoin is neither. Bitcoin’s price behavior more resembles a Realestate craze.

Rafi, where is your biblical commentary? I thought that is what I was getting when I paid the subscription.